Mineral Finance: A Critical Year for the Mineral Industry

It was a year characterized by starts and stalls to pandemic recovery efforts. The impacts felt within the real economy and global financial markets in 2021 played a significant role in metal price trends, as well as financing for mineral exploration and associated expenditure levels.

Reducing global emissions, the supply of minerals critical to this transition, as well as those of strategic importance to various regions around the world have been dominant issues over the past year.

These issues may be setting the stage for a shift in industry activity in a post-pandemic environment. The visuals below outline relevant trends and provide insight on key markers within the mineral exploration and development sector.

Mineral Finance 2022 is broken into the following sections. Click one to jump ahead.

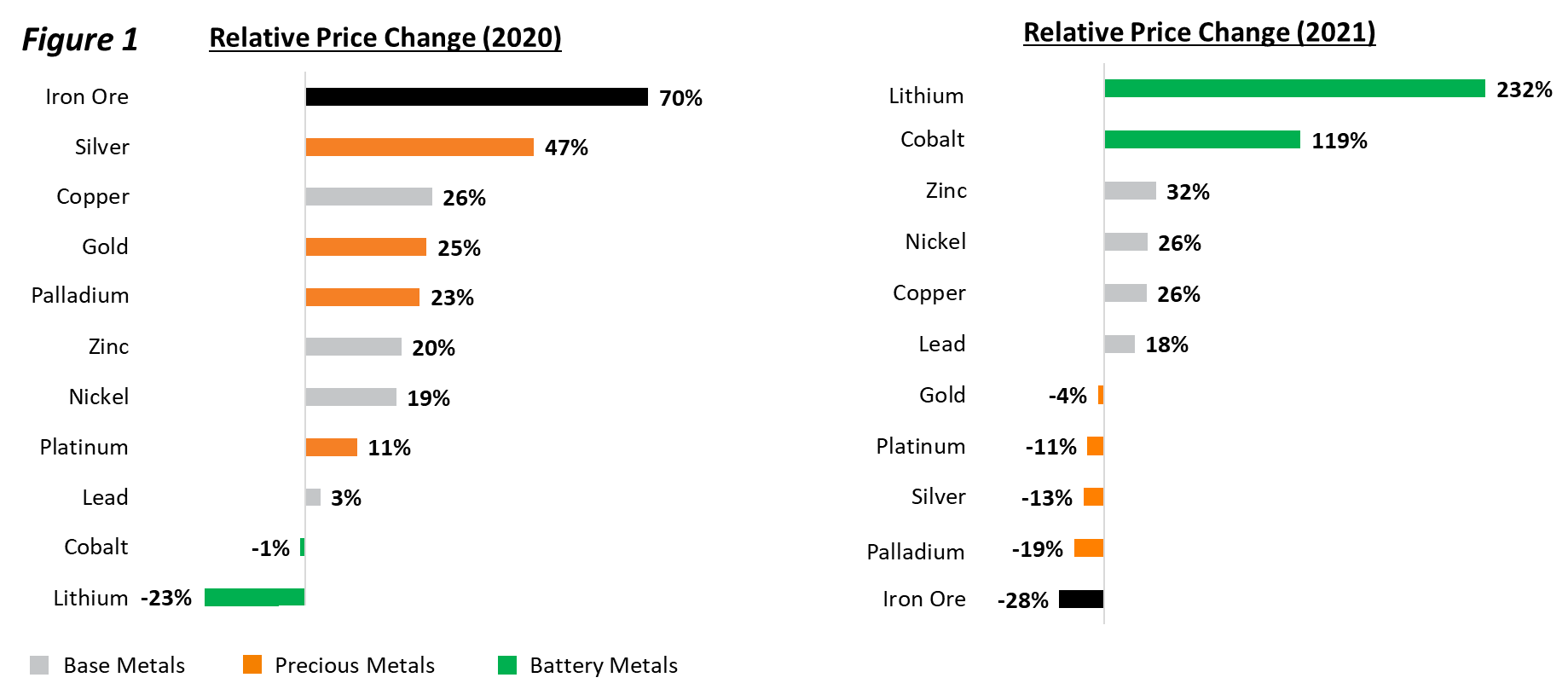

Figure 1 represents the year-over-year price change of a broad suite of the metals in 2020 and 2021 for comparison.

The coloured bars in the figure reveal how metals at the top and bottom end of the spectrum switched positions in 2021, compared to 2020. After trending downward for three consecutive years, key battery metals (cobalt, lithium) led the pack, while iron ore and precious metal prices ended up in negative territory, relative to the start of the year.

Base metals kept the positive momentum in 2021 in another solid year of material price increases.

The following three charts detail price dynamics of key metals. Looking more closely at the spot price dynamics of these metals in 2021.

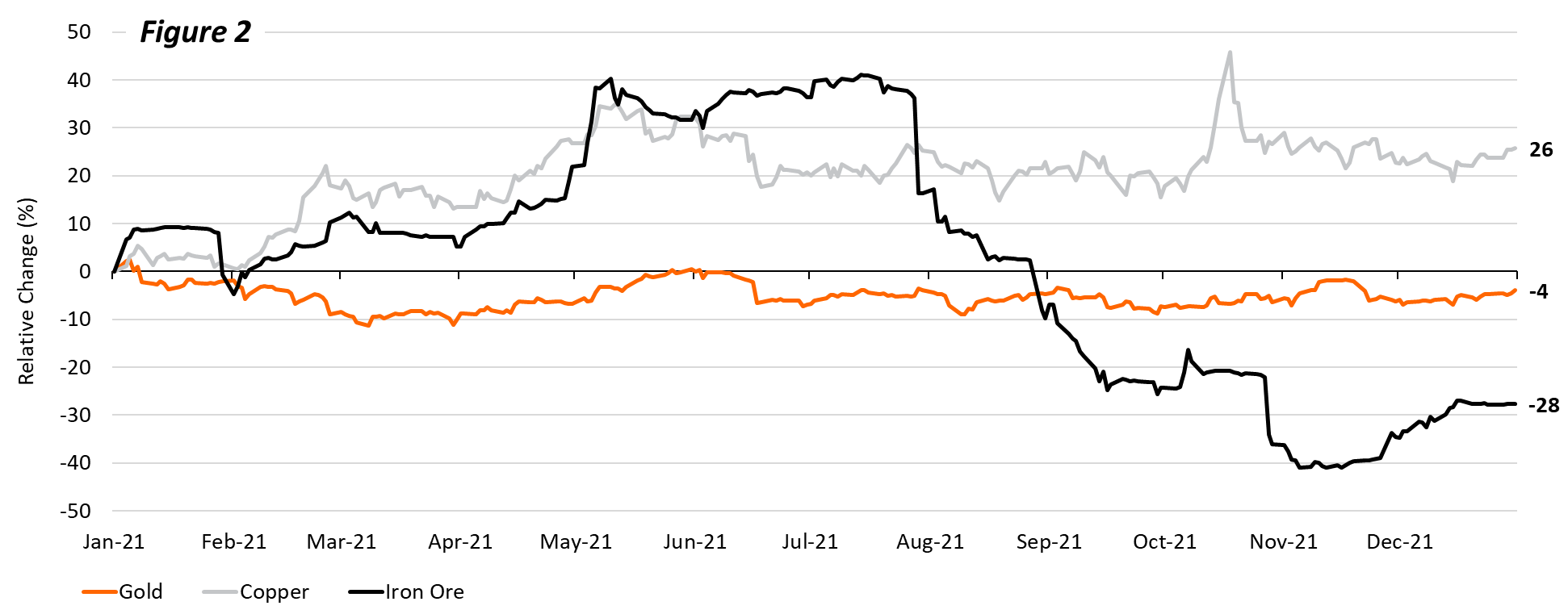

Figure 2

Figure 2 reveals stark differences.

Industrial metals like copper and iron ore benefited from initial signs of economic recovery in early 2021 with prices appreciating for both to reach all-time highs by midyear. However, China’s pledge to reduce iron ore consumption in July 2021 led to a price collapse by year-end. Copper, with a broader and more significant global consumption base, maintained higher prices through to the end of the year, continuing into 2022.

In contrast, gold went sideways in 2021 as spot prices kept within a narrow range and ended the year down approximately 4%. The modest decline may reflect the impact of vaccines and economic stabilization taking hold within the global economy after reaching an all-time high in August 2020.

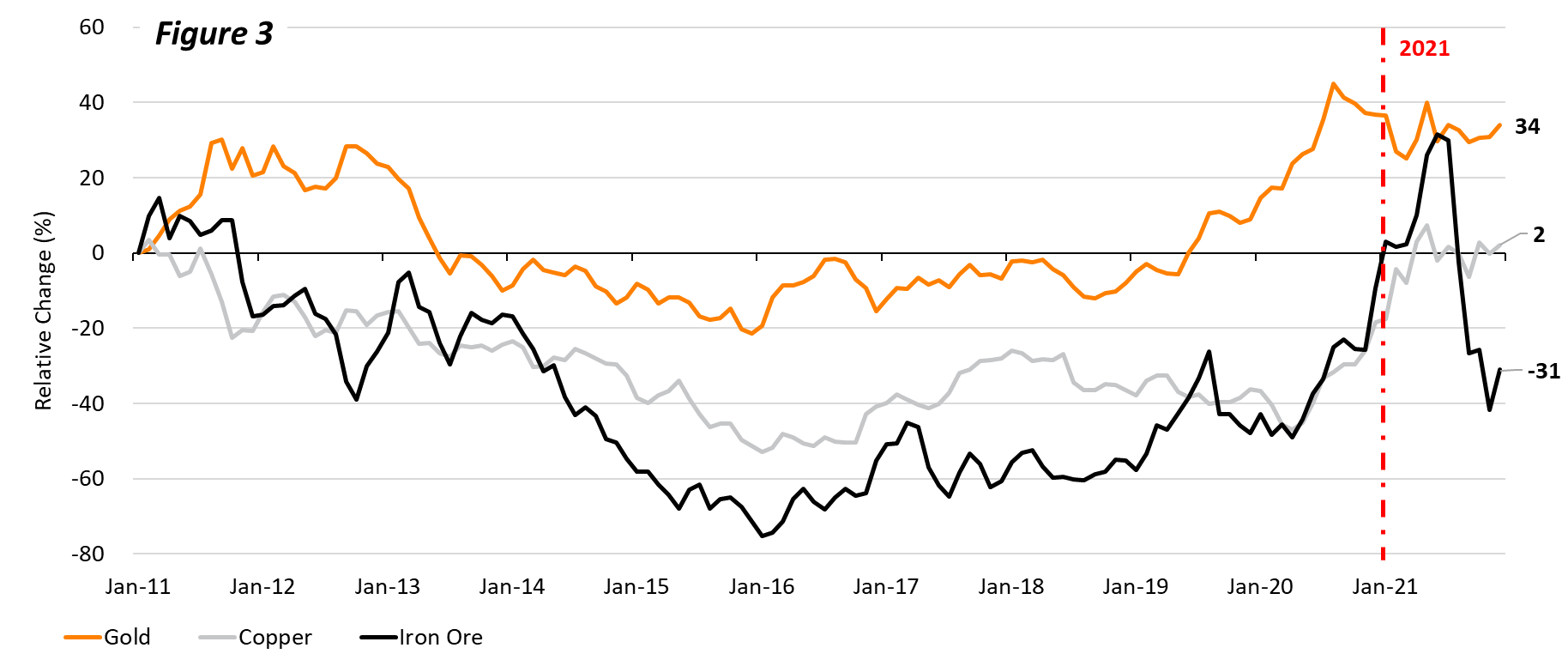

Figure 3

Looking back over the past decade, Figure 3 presents long-term price trends of key commodities based on monthly average prices.

The longer-term view emphasizes the peaks reached by copper and iron ore in 2021 and by gold in 2020. Over the whole timeframe, gold appears as the clear winner.

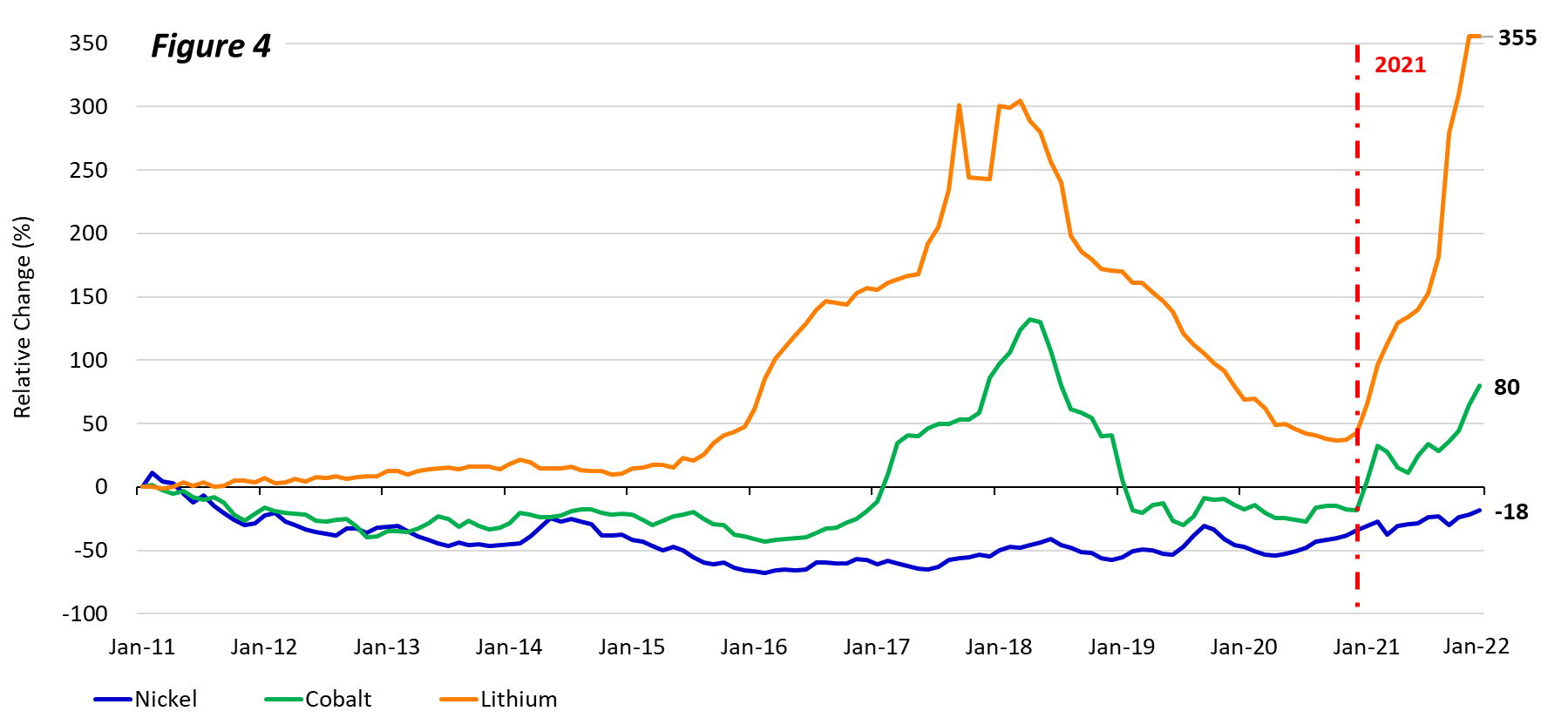

Figure 4

Figure 4 presents the long-term price trends of several key battery metals.

After three consecutive years of downward price trends, battery metals found a bottom towards the end of 2020. With most economies around the world picking up pace by mid-2021, and with eyes looking increasingly towards ambitious infrastructure and emission reduction plans by various governments, cobalt and lithium prices have surged upward.

Figure 4 shows how lithium prices shot past 2018 levels and while cobalt did not do the same, its price nearly doubled in 2021.

The large differential in price appreciation may reflect supply chain concerns around cobalt and risks associated with roughly 50% of the world’s current supply coming from production in the Democratic Republic of Congo (DRC). This has caused some large Electric Vehicle (EV) manufacturers to look to nickel or other minerals as an alternative to reduce the amount of cobalt used in batteries.

The price trend of nickel is noticeably lackluster compared to the other two metals in Figure 4. This may be a result of the fact that despite the increase in use of nickel for batteries, its main use remains in the production of stainless steel. We have seen nickel fluctuate significantly in the first quarter of 2022 as global supply concerns and market imbalances have pushed the nickel price above $20 per pound – a level not seen since 2007.

Global Mineral Industry Financing

Figure 5

Figure 5 shows global financing for the mineral sector since 2011, segmented into equity and debt.

Despite debt financing hitting a decade low, Figure 5 shows equity financing up significantly year-over-year in 2021 and on par with levels raised from 2012-2017. This could be an effect of appreciating metal prices driving broader margins and high equity valuations throughout 2021, and issuers increasingly choosing to raise equity over debt in active capital markets.

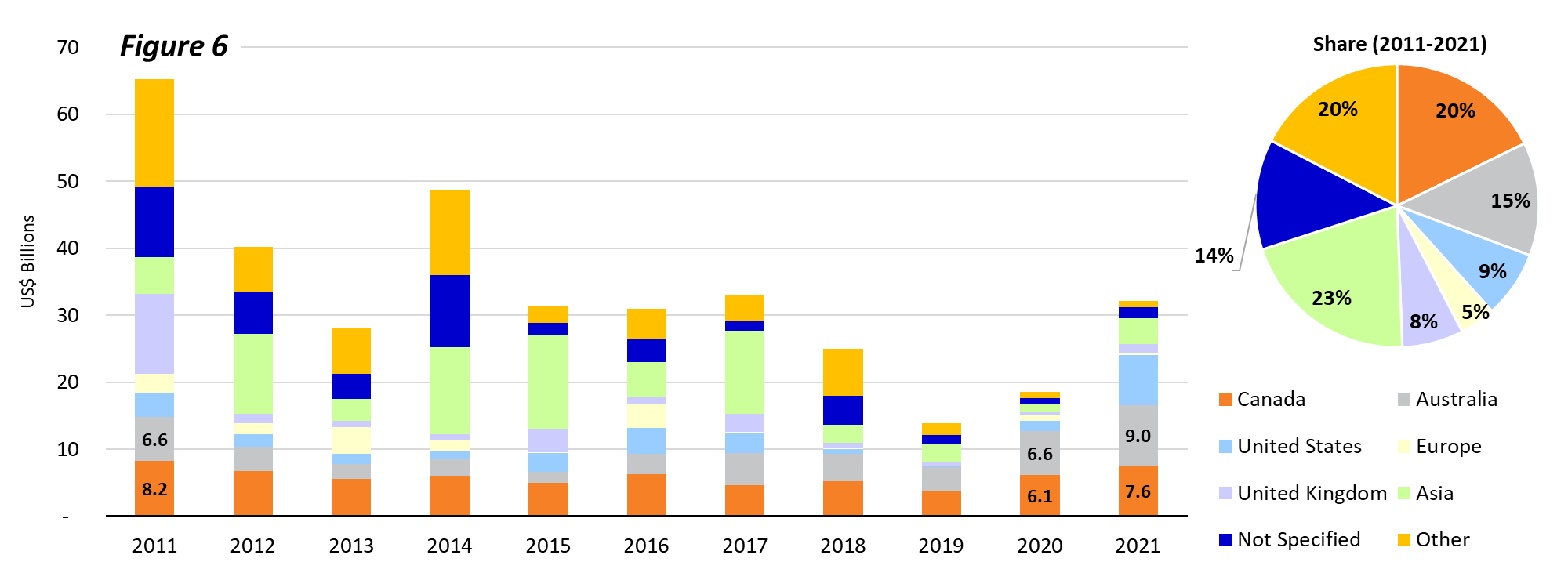

Figure 6

Figure 6 focuses closely on equity, disaggregated by region, based on where funds were raised.

After a notable rebound in 2020, the total amount of equity raised by the mineral sector continued to climb in 2021, increasing by approximately 73% year-over-year.

The aggregate amount raised in markets outside Canada almost doubled, significantly exceeding the roughly 23% increase in equity financing on Canadian exchanges over the same timeframe. This caused Canada’s relative share of equity market activity to decline in 2021

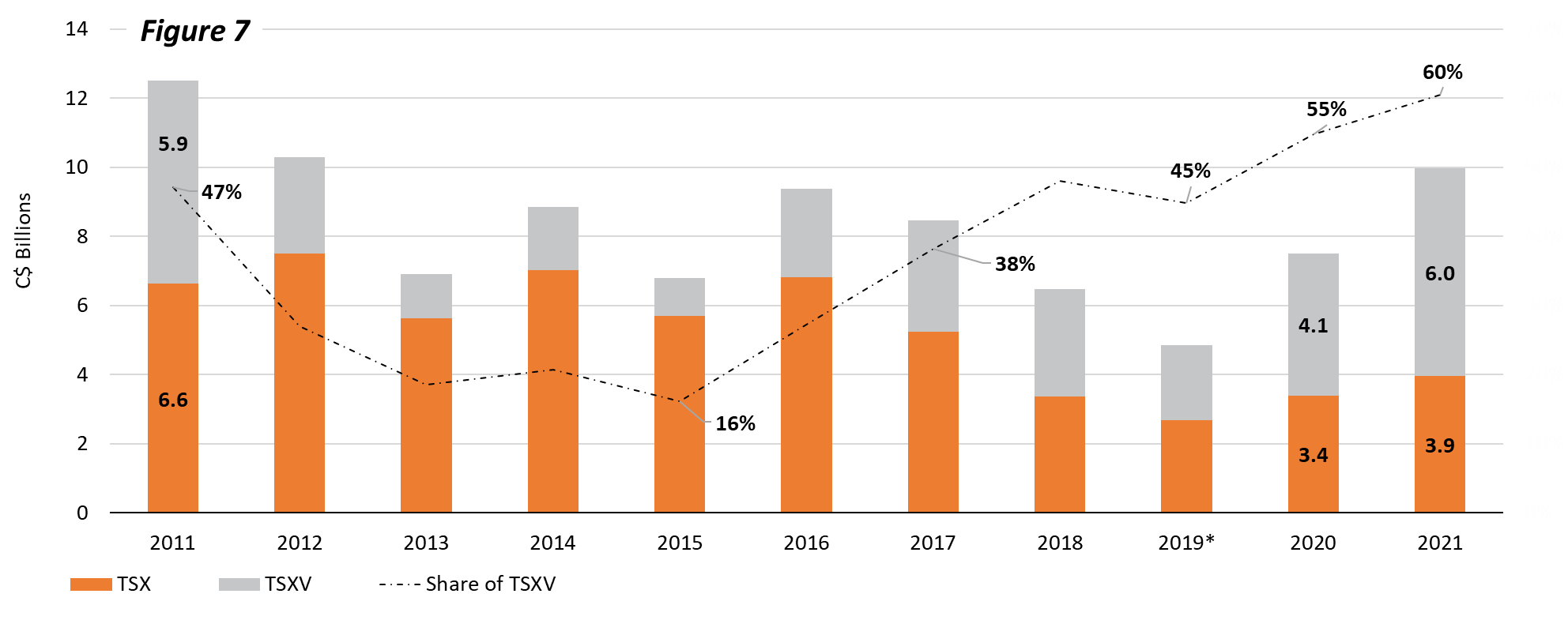

Financing on Canadian Exchanges

Figure 7

Figure 7 disaggregates between funds raised on the TSX and TSX Venture (TSXV) exchanges.

In 2021, the amount raised on the TSX and TSXV combined to reach almost $10 billion (CAD)—the most active year since 2012. The proportion of total funds raised by venture issuers (grey bars) climbed to 60% in 2021, in line with an upward trend from a 2015 low-point. In fact, TSXV issuers raised more funds last year versus 2011.

For TSX issuers, the total amount raised from equity financings increased for the second year in a row. However, activity on this Canadian exchange remains well below pre-2018 levels.

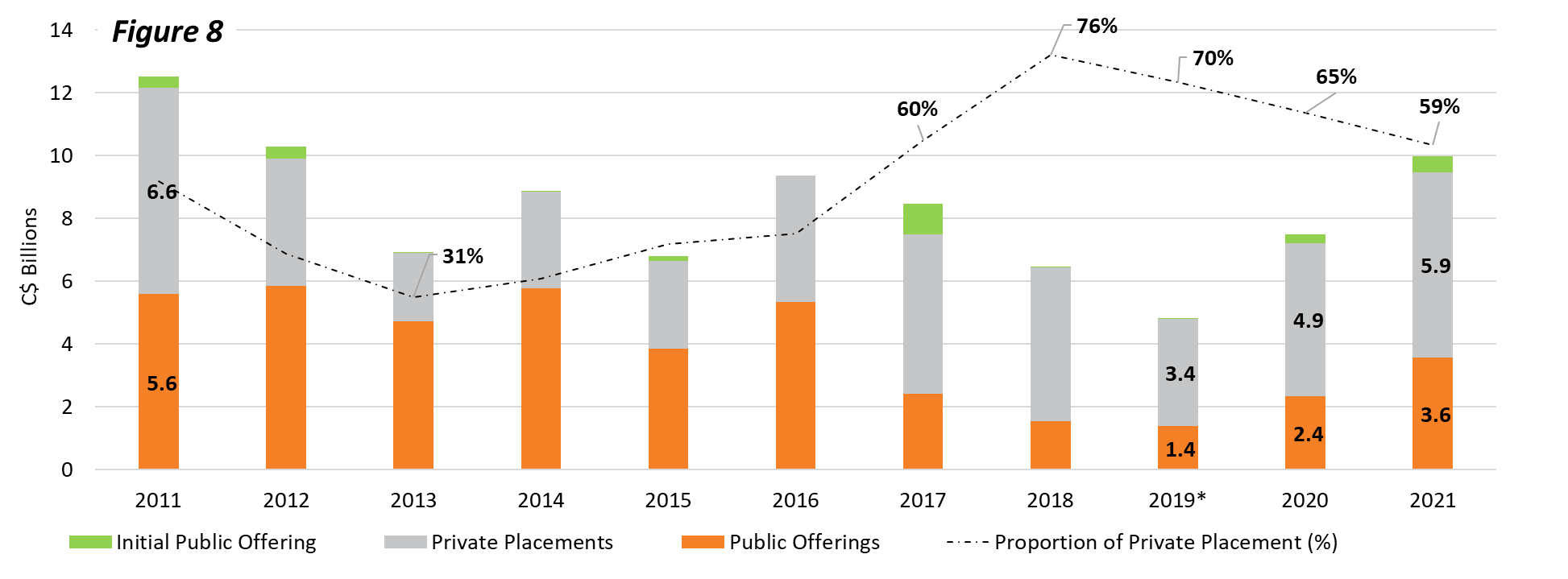

Figure 8

Figure 8 outlines TSX/TSV financings disaggregated by the type of equity being issued into the market.

In 2021, the total amount of funds raised via private placement (grey bars) reached levels not seen in a decade. The dashed line shows that the proportion of private placements declined for a third straight year. It is positive to see the total amount raised by public offerings and IPOs have climbed by a substantial amount over the last two years.

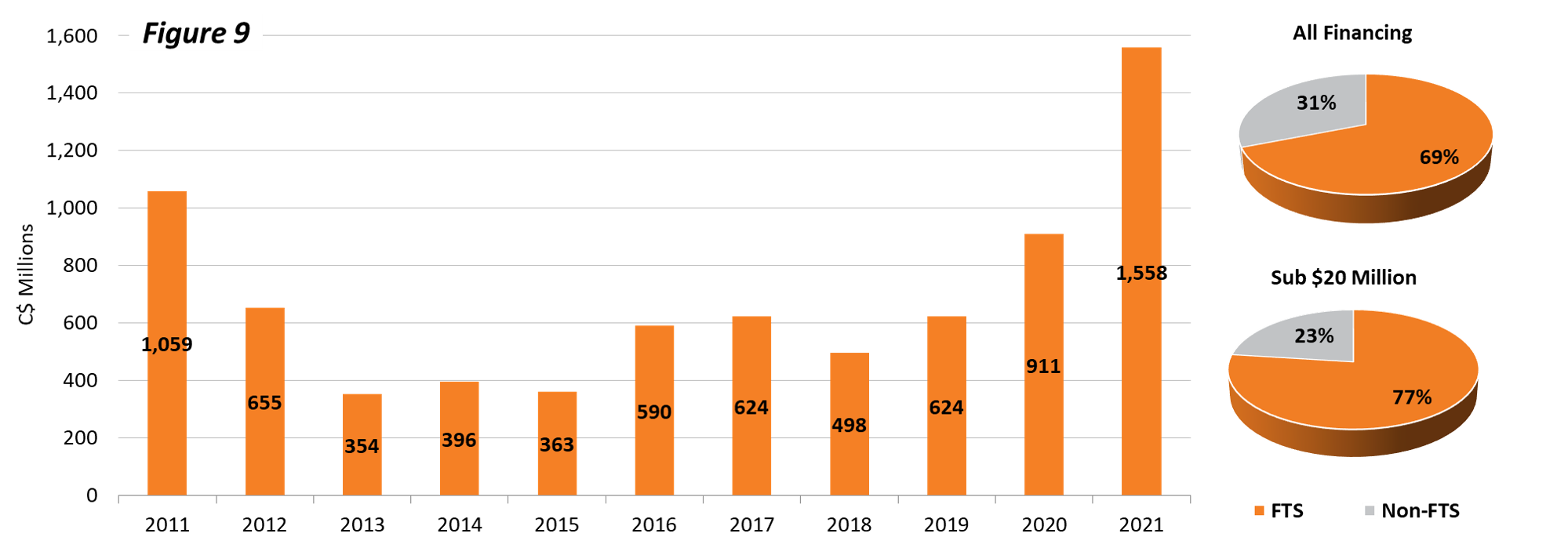

Figure 9

Figure 9 presents flow-through share (FTS) funds raised on Canadian stock exchanges, which are required to be dedicated towards domestic mineral exploration.

FTS have long represented a cornerstone of Canadian competitiveness and the mechanism consistently generates significant domestic exploration activity each year. This fact was reinforced in 2021 as it represented an all-time high with respect to the amount of funds raised via FTS issuances.

Based on PDAC analysis of Canadian financings, roughly 70% of all funds raised for domestic exploration over the past decade have been through the FTS mechanism. Moreover, the proportion of funding sourced from FTS increases to almost 80% for smaller transactions (sub-$20 million), which is common among junior exploration companies.

Exploration Activity & Expenditures

The last series of figures (10-14) provide a snapshot of exploration activity by outlining expenditures within the industry over time.

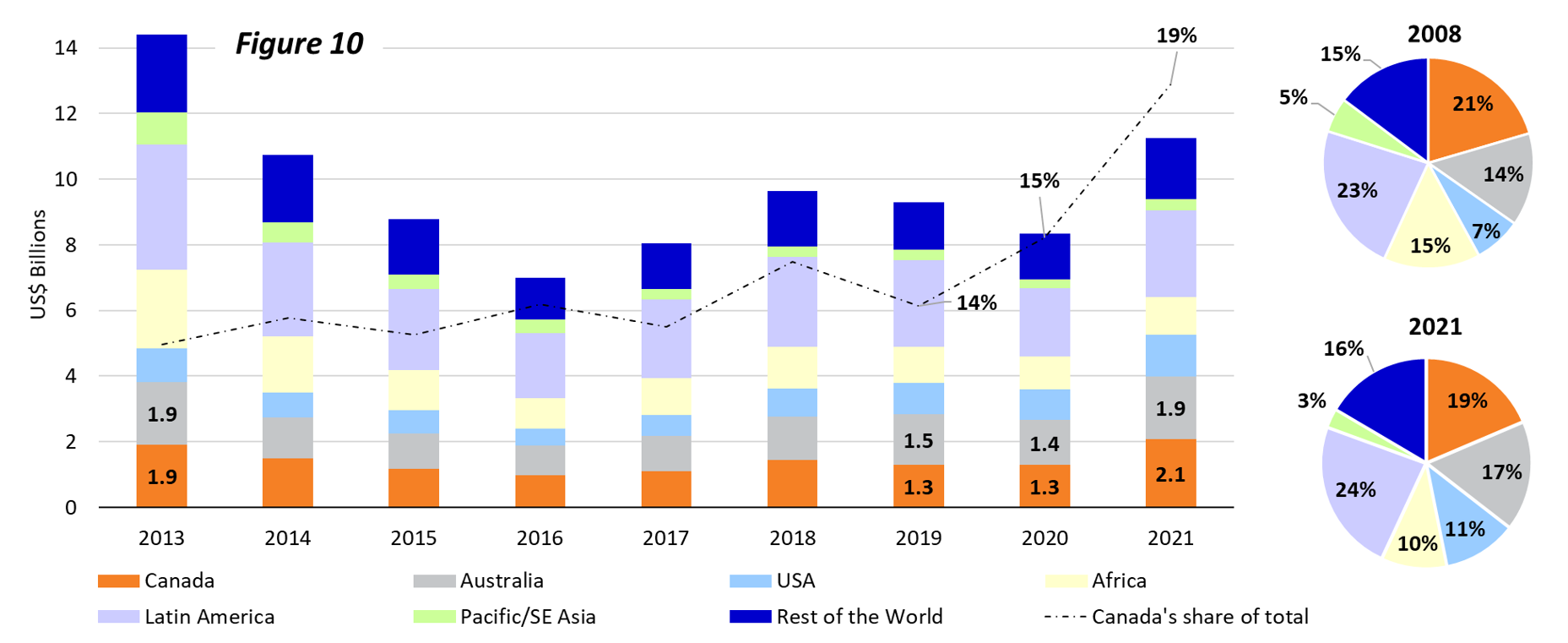

Figure 10

First, Figure 10 presents global exploration expenditures based on the region where they are spent.

The bar chart in Figure 10 reveals an estimated 35% increase in global exploration activity in 2021 compared to the year prior—the first increase in several years. This upswing is largely attributable to the upward price trend for most commodities, which sparked a robust financing environment in 2020.

Exploration spending in Canada jumped more than 60% in 2021 versus 2020, and the proportion of global expenditures directed towards Canada moved up to approximately 19%, well above the low-point recorded in 2013. This increase led Canada to reclaim its position as the top global destination for mineral exploration (Australia held it the two years prior). However, as can be seen in the pie chart in Figure 10, Canada has yet to reach the proportion of global activity recorded in 2008.

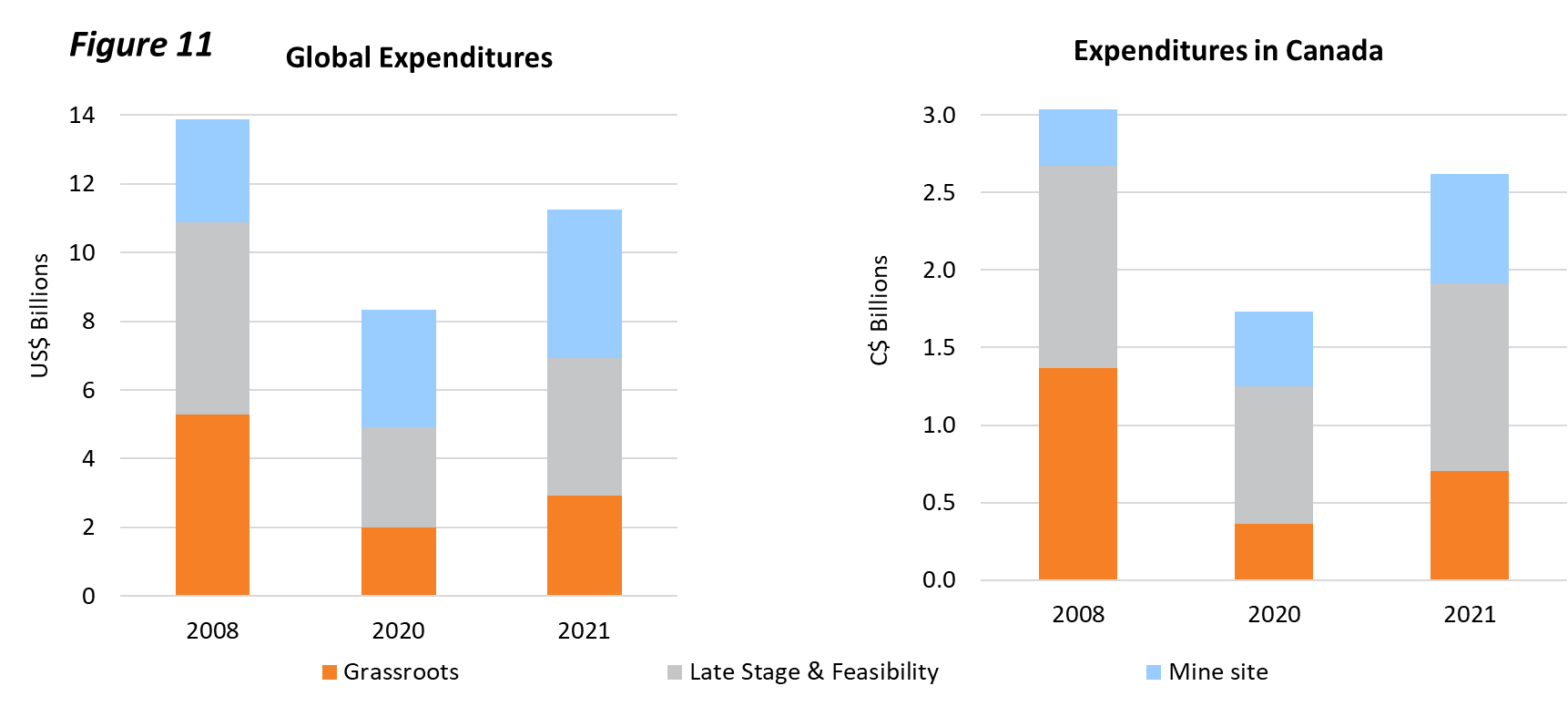

Figure 11

Figure 11 presents global and domestic exploration spending in 2008, 2020 and 2021 disaggregated by project stage.

Grassroots mineral exploration is the earliest stage of activity conducted by individuals and companies in the field. It is the primary source of new discoveries, both those within traditional market segments like gold and copper, as well as minerals that are increasingly associated with green and low-emission technologies. With this in mind, it is positive to see year-over-year increases for grassroots expenditures.

Though, spending levels remain well below activity recorded in the previous decade and hints that discovery rates are declining around the world.

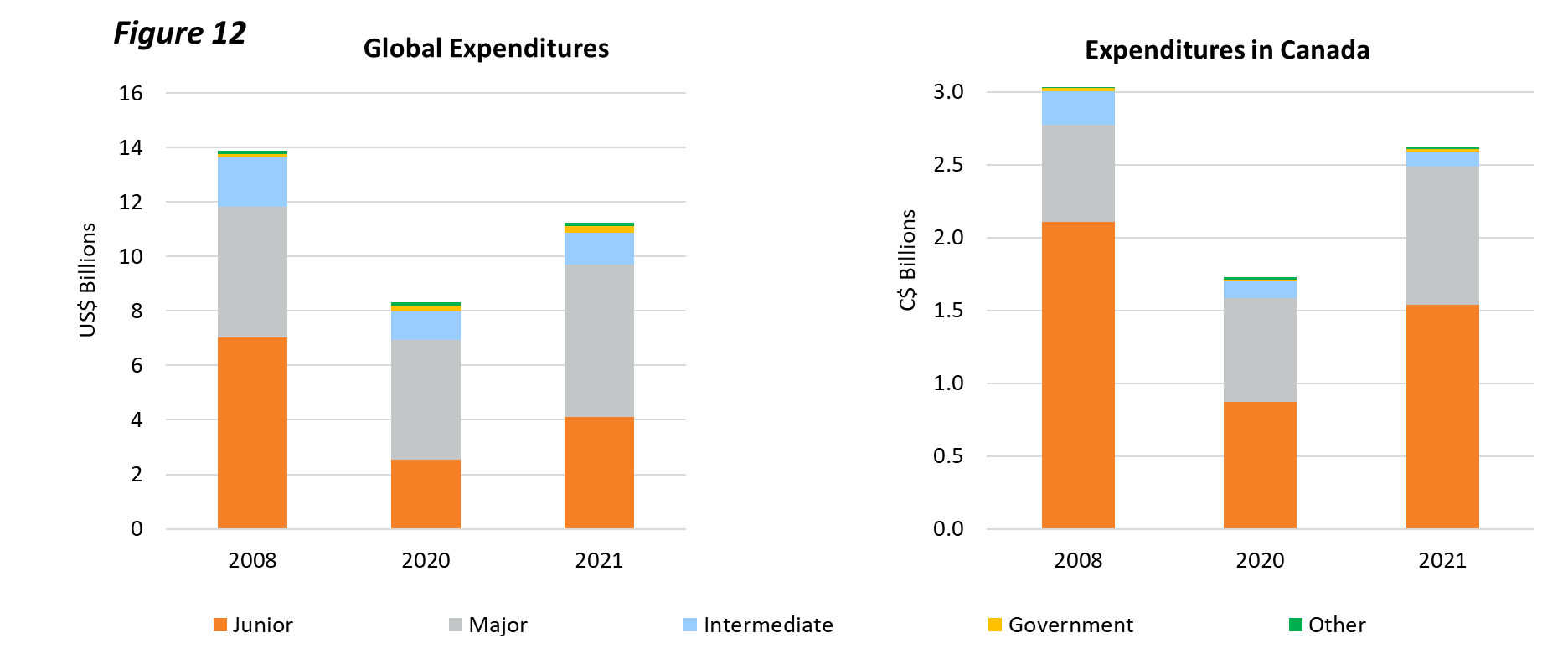

Figure 12

Figure 12 outlines exploration expenditures by company type for the years 2008, 2020 and 2021.

The balance of spending between different-size companies and company types is an important measure when assessing activity levels and the potential for new discoveries to be uncovered.

The bars above break down exploration spending and show how junior exploration spending declined significantly between 2008 and 2020, both globally and within Canada. While 2021 spending levels have not climbed back to 2008 levels, it is positive to see junior spending up in Canada and abroad, which opens the potential for resource and economic growth.

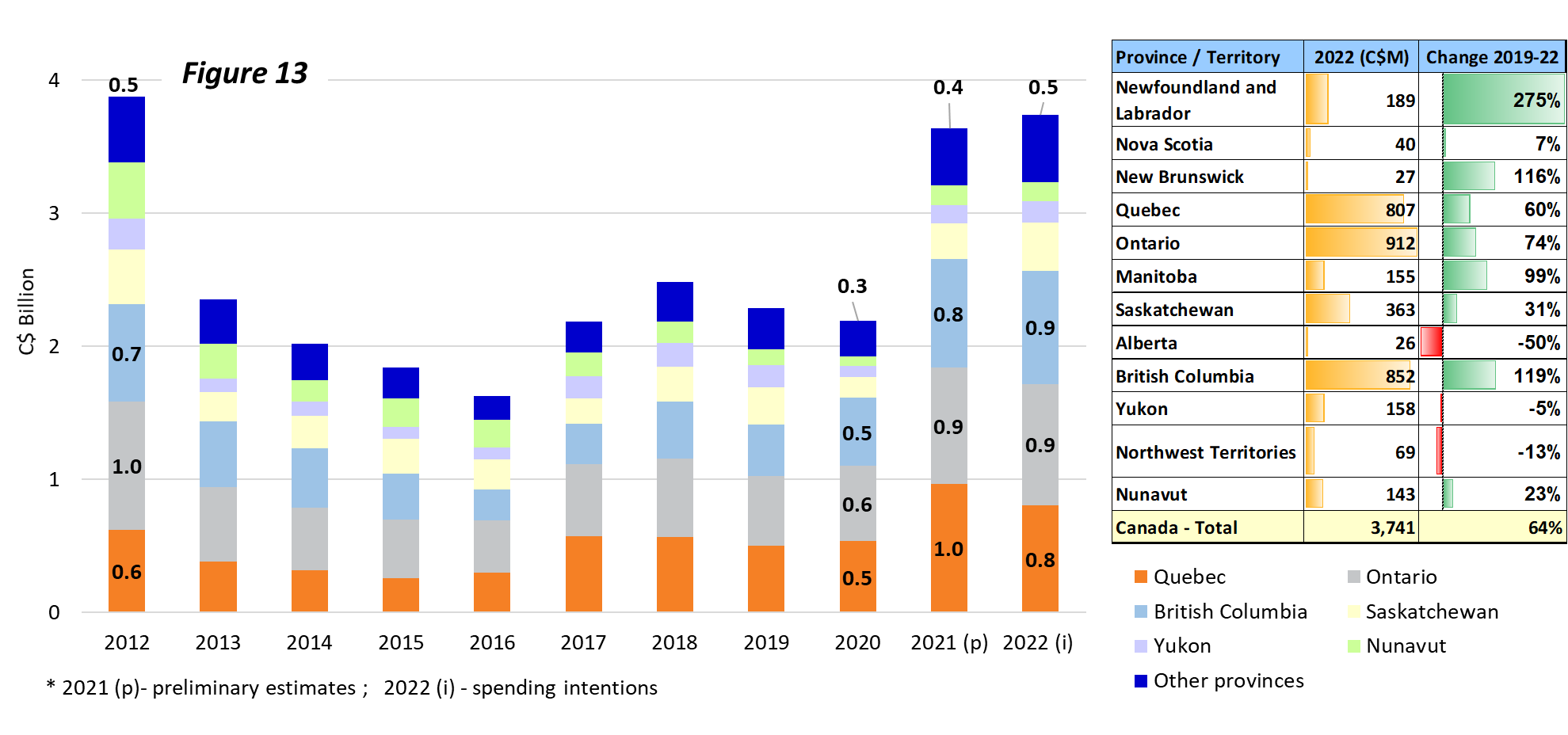

Figure 13

The last set of charts detail exploration expenditures in Canada over the last decade. Figure 13 presents exploration expenditures in Canada by province, and includes initial spending intentions for 2022.

Canada recorded a year-over-year increase in exploration spending of more than 65% in 2021, and activity for the current year is set to increase again, although only by a marginal amount. It is noticeable that expenditures over these past two years are the highest reported since 2012. Recalling the FTS financing chart (Figure 9) in the previous section, we can see a direct correlation in the jump in FTS deals and the level of exploration activity across the country.

Looking at spending estimates, Ontario, British Columbia and Quebec will continue to dominate domestic exploration activity. While Ontario and B.C. are projecting expenditures will increase roughly 4% and 5% respectively in 2022 versus 2021, activity in Quebec is set to decline approximately 16% over the same timeframe.

It can also be seen from the table on the right of Figure 13 that there are a number of regions in Canada where exploration activity has not rebounded to pre-pandemic levels. A drop in activity has been recorded in the Northwest Territories, Yukon and Alberta between 2019 to 2022 with Nunavut and Saskatchewan also falling short of the rebound indicated in other regions over the same period. The slow-down in the territories highlights how infrastructure deficits and the lack of access to a region can significantly impede economic activity and, in this case, economic recovery.

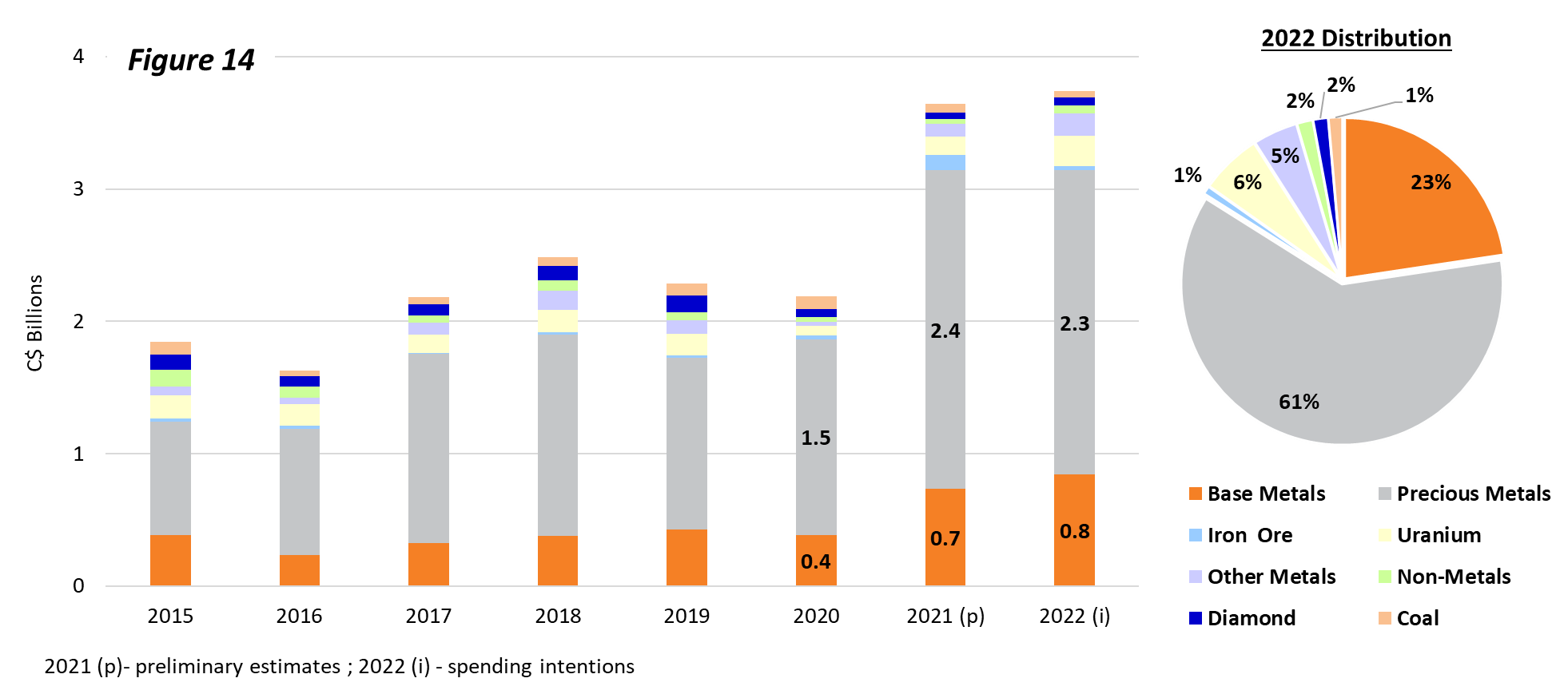

Figure 14

Lastly, Figure 14 presents Canadian exploration expenditures in Canada, disaggregated based on commodity type.

It is clear that precious metals (grey bars) dominate activity within Canada and gold exploration receives the majority of funding within that segment. Base metals, such as copper and nickel, rank number two in terms of annual activity and, on average, account for about 20% of annual Canadian spending.

In looking to identify how much domestic spending is being directed towards less-traditional critical minerals like cobalt and lithium, we see that less than 3% of exploration spending in 2021 was directed towards ‘Other Metals’. While it is positive to see this figure increase in 2022, it still represents less than $100 million of the nearly $3.5 billion in estimated exploration spending in Canada this year. The lack of exploration activity in this market segment only reinforces the need for governments across the country to work collaboratively on policy tools that boost Canada’s ability to become the supplier of choice in the transition to a low-carbon future.

Sources

Numbers are based on PDAC data sourced from S&P Global Market Intelligence, TMX Group and Natural Resources Canada (NRCan).

Metal Prices (Figures 1-4): S&P Global Market Intelligence

Financing (Figures 5-9): Figures 5-6: S&P Global Market Intelligence Figures 7-8: TMX Group Figure 9 – TMX Group, S&P Global Market Intelligence