Continued monetary contraction policies by central banks around the globe in 2023, along with further escalations of geopolitical tensions, sparked concerns for the health of global economy.

The demand for raw materials declined, constituting a headwind to metal prices, and mineral exploration and development companies saw further reduction in the capital available to them.

At the same time, the launch of various government incentives for critical minerals aimed at supporting the energy transition provided significant incentive to look for these materials, at the expense of traditional metals such as precious metals.

This page presents the key developments around metal prices, financing and mineral exploration activity in Canada and around the world.

Mineral Finance 2024 is broken into the following sections. Click one to jump ahead.

The series of charts that follow will outline some relevant price trends throughout 2023 and the first half of 2024 and will give some insights into what to expect in the second part of the year.

Figure 1 presents a comparison of the year-over-year (YOY) price change for a suite of metals in 2022, 2023, and the first half of 2024.

In 2022 and 2023 there was a widespread decline in the demand for raw materials. However, the first half of 2024 saw a recovery in the prices of base metals as well as precious metals like gold and silver.

Uranium was the best performer in 2023, driven by the increase in expected demand for nuclear energy along with a limited supply. Iron ore prices initially responded positively to incentives for real estate developers during the last few months of 2023. However, despite China’s efforts, the ongoing overcapacity in steel production reduced the demand for iron ore, causing it to be the worst performer in the first half of 2024.

For industrial metals (primarily base and battery metals) the figure above depicts a volatile price environment influenced by two conflicting dynamics. In the short term, metal prices have been responding in recent years to fears of an economic recession that may reduce the demand for raw materials. Conversely, there are expectations for a significant long-term increase in demand for industrial minerals due to the energy transition and other technological developments, such as materials needed for the artificial intelligence revolution.

Figure 2

Figure 2 shows the spot prices of gold and copper, the key precious and base metals in terms of market value, from 2020 until early 2024.

After remaining relatively stable throughout most 2021 and 2022, gold’s price began an upward trend since late 2022. This increase has been driven by high levels of central bank purchases, expectations for upcoming interest rate cuts, and increasing geopolitical tensions. Gold continued its really well into the second half of 2024, and as of late August 2024, gold's price is in all time high, hovering around $2500 per ounce.

Copper, on the other hand, experienced a decline in price starting in mid-2022 due the economic monetary contraction. However, in 2024, copper prices surged. This rally was fueled by supply issues, such as the production halt at Cobre Panama, and the growing realization of long term demand for copper, driven by the shift to a low-carbon economy and other technological developments.

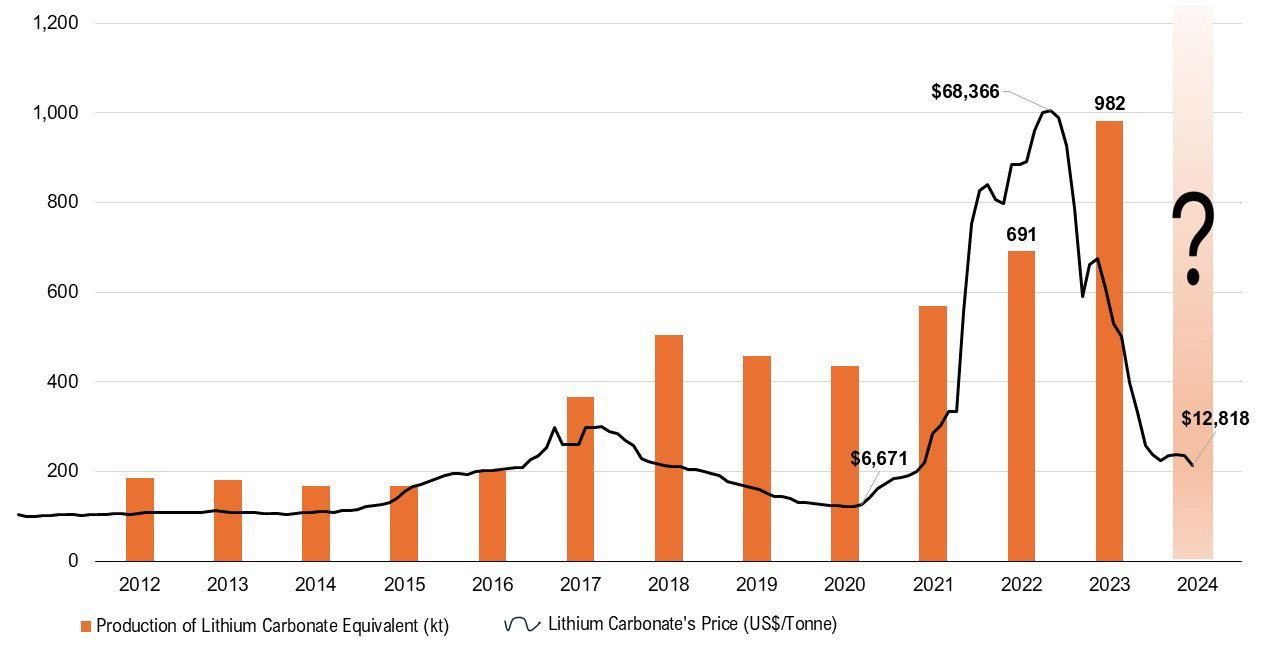

Lithium, the key battery metal, was the worst performer in 2023, in a stark contrast to its strong performance in 2021 and 2022, when prices soared due to strong electric vehicle (EV) hype. As a result, mine production increased in 2023 by 40% YOY. The increase in production, coupled with a lower-than-expected rate of EV penetration to auto markets, created supply surplus and caused the price of lithium to collapse.

Figure 3

Figure 3 shows a long-term view of lithium’s price and production, and illustrates the dynamics noted above.

Cobalt and lithium prices have moved largely in-step over the last 5+ years but that trend was most definitely broken in 2022 as Figure 3 on the right shows. Note the significant change in the scale of the y-axis from Figure 2 required to plot the climb in lithium over the last 18 months. The divergence that began in 2021 marks a significant split that most likely results from the differing future demand expectations that we noted above.

We can see a much less volatile nickel price over the same period as the metal’s use in batteries still only represents a small portion of annual consumption. The staggering increase in the demand for lithium-ion batteries has not affected the price of nickel in a material way to this point but this could change in the not-too-distant future as new battery tech continue to be developed and refined.

Investment Activity

Figure 4

The collapse in the prices of most metals throughout 2023 along with the continued contraction of the global economy reduced the availability of capital and exacerbated the financing challenges felt by mineral issuers. Next, figures 4-8 present different aspects of mineral financing.

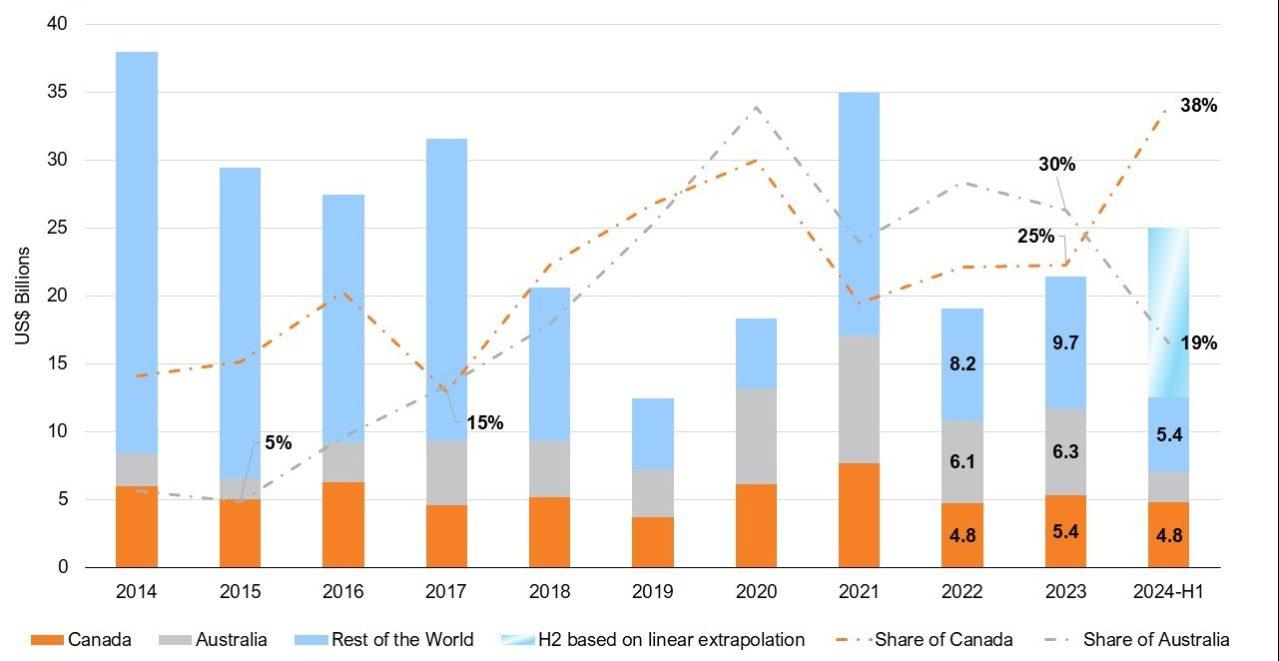

Figure 4 presents the global equity financing for the mineral sector raised in the two leading global financing hubs, Canada and Australia, versus funds raised elsewhere.

Global equity financing increased in 2023 by 12% YOY, but it was below the ten-year average of US$25 billion. While Canadian exchanges still lead most around the world in attracting new investments into the mineral industry, Australia has ‘out-raised’ domestic Canadian markets in recent years. The Australian market took top spot for equity raises in 2023, but total financings on the Australian Stock Exchange (ASX) were down YOY. The gap between Canada and Australia in 2023 was the narrowest recorded in four years, and in the first half of 2024 a reversal of this trend was seen.

Figure 5

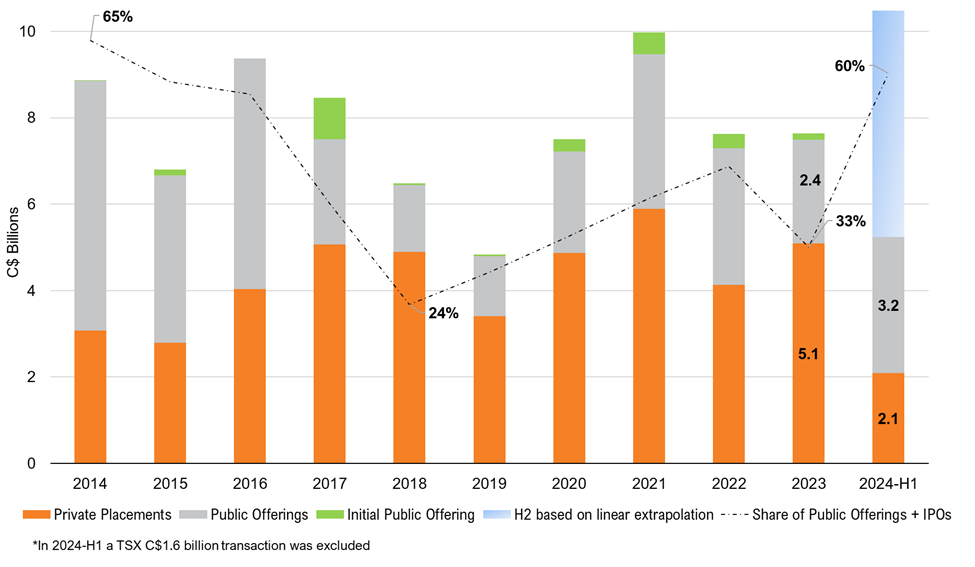

Putting the spotlight on key domestic stock exchanges, Figure 5 presents equity financing in the Toronto Stock Exchange (TSX) and the venture exchange (TSXV), disaggregated by public vs. private funding (note the different currencies (US$ vs. C$) and data sources in Figure 4 versus Figures 5-8).

In 2023 the level of total equity raises was similar to that of 2022, but the internal composition changed significantly. After four consecutive years of increasing the proportion of public funds (public offerings and IPOs), 2023 saw a reversal of this trend. This is concerning because, while a private placement is a relatively low-cost fundraising solution, it doesn’t enable wide-spread distribution of the stocks and therefore doesn’t help the company achieve a healthy increase in its investor base. The first half of 2024 was more encouraging as significantly more equity was raised with higher proportion of public funds, despite excluding an outlier public offering transaction.

Figure 6

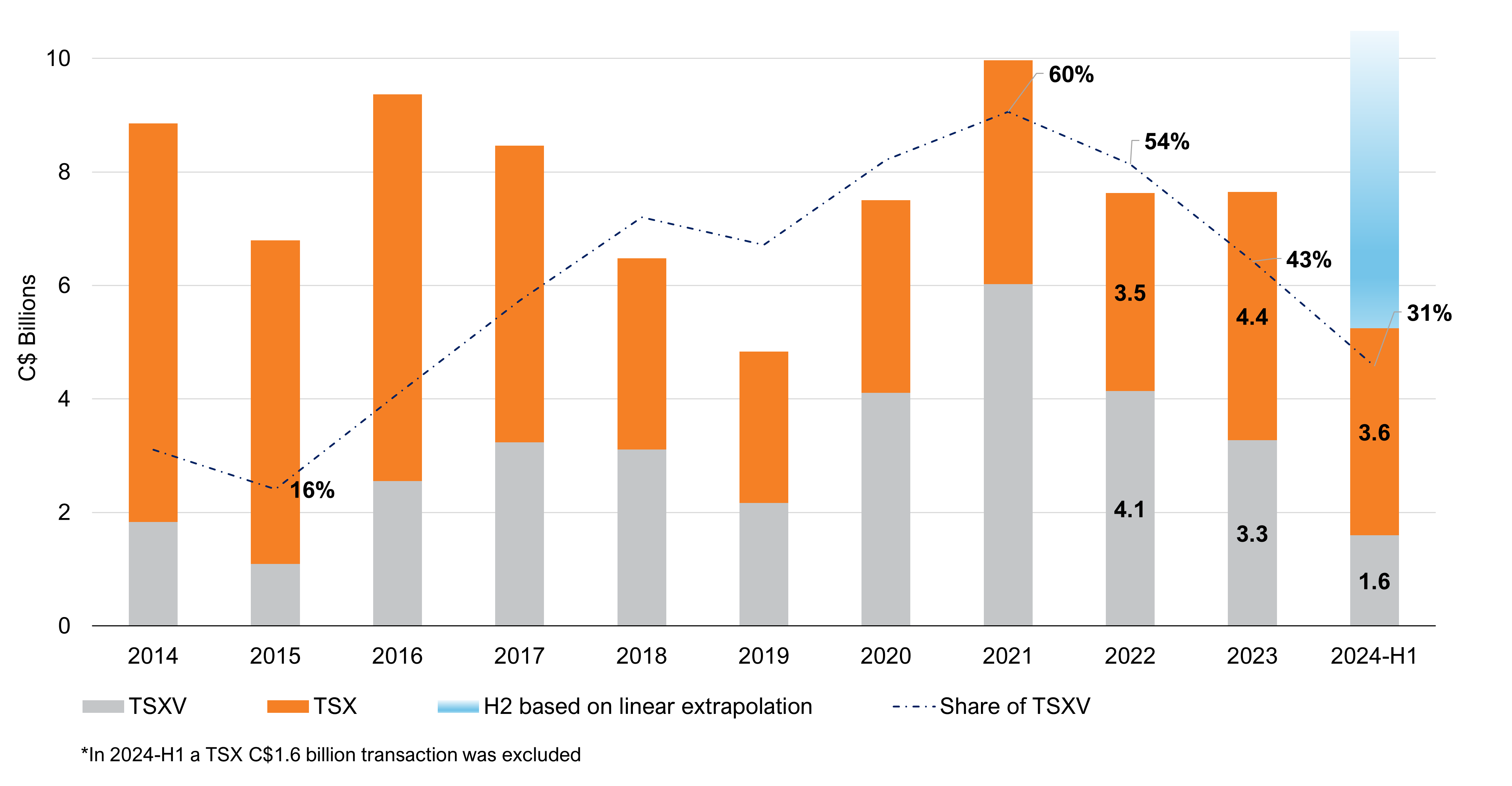

Figure 6 shows the split in equity investment for mineral exploration, development, and mining companies on the TSX and TSXV Exchanges.

The TMX data shows total equity raised in 2023 was only slightly above 2022’s level, but the internal composition changed as the share of TSX listed issuers increased at the expense of investments into smaller companies listed on the Venture exchange. This is likely a sign of the availability of risk capital drying up as broader markets weaken.

This trend continues well into the first half of 2024, with funding on the venture exchange declines in both absolute and relative terms.

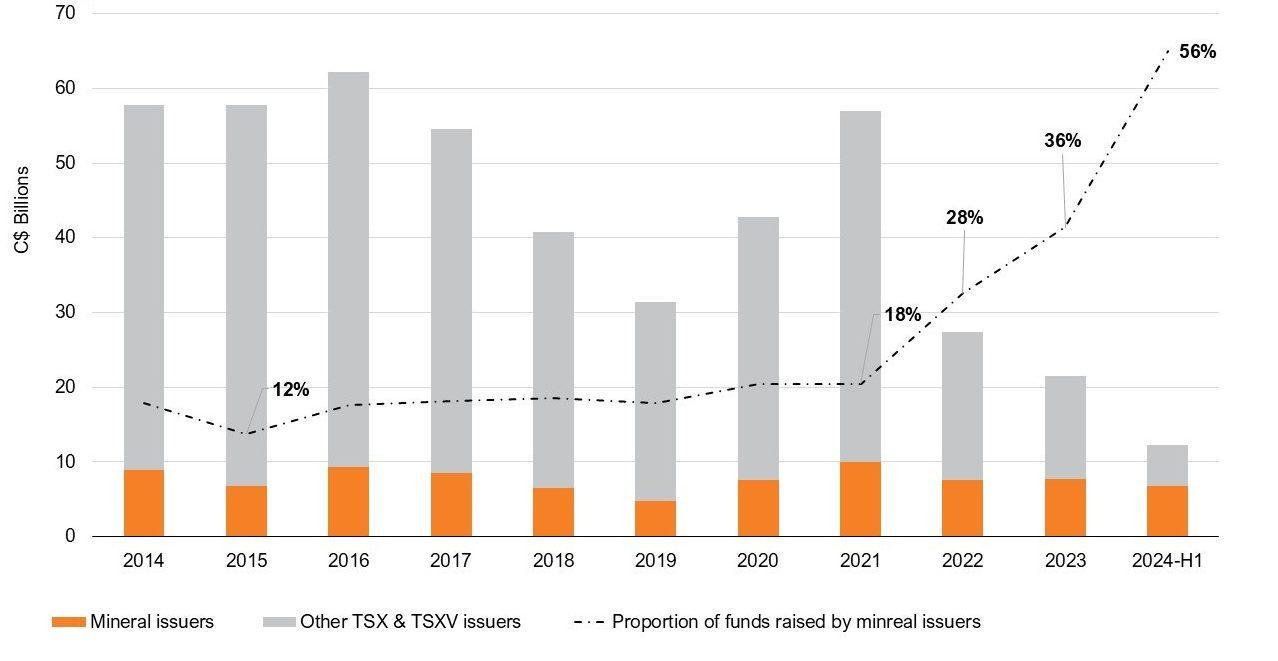

Figure 7

Figure 7 presents the equity raised by mineral issuers out of total equity financing obtained via TSX & TSXV.

While funds raised by mineral issuers (orange bars) have been declining since 2021, a steeper decline in other sectors’ financing caused the proportion of funds raised by mineral issuers to increase significantly, from below 20% until 2021 to 36% in 2023, and a staggering 56% in the first half of 2024.

The relative strength of mineral issuers in recent years, while other capital sources have been drying up, emphasizes the importance of fiscal incentives that support various stages along the mineral supply chain, such as the Flow-through Share (FTS) regime.

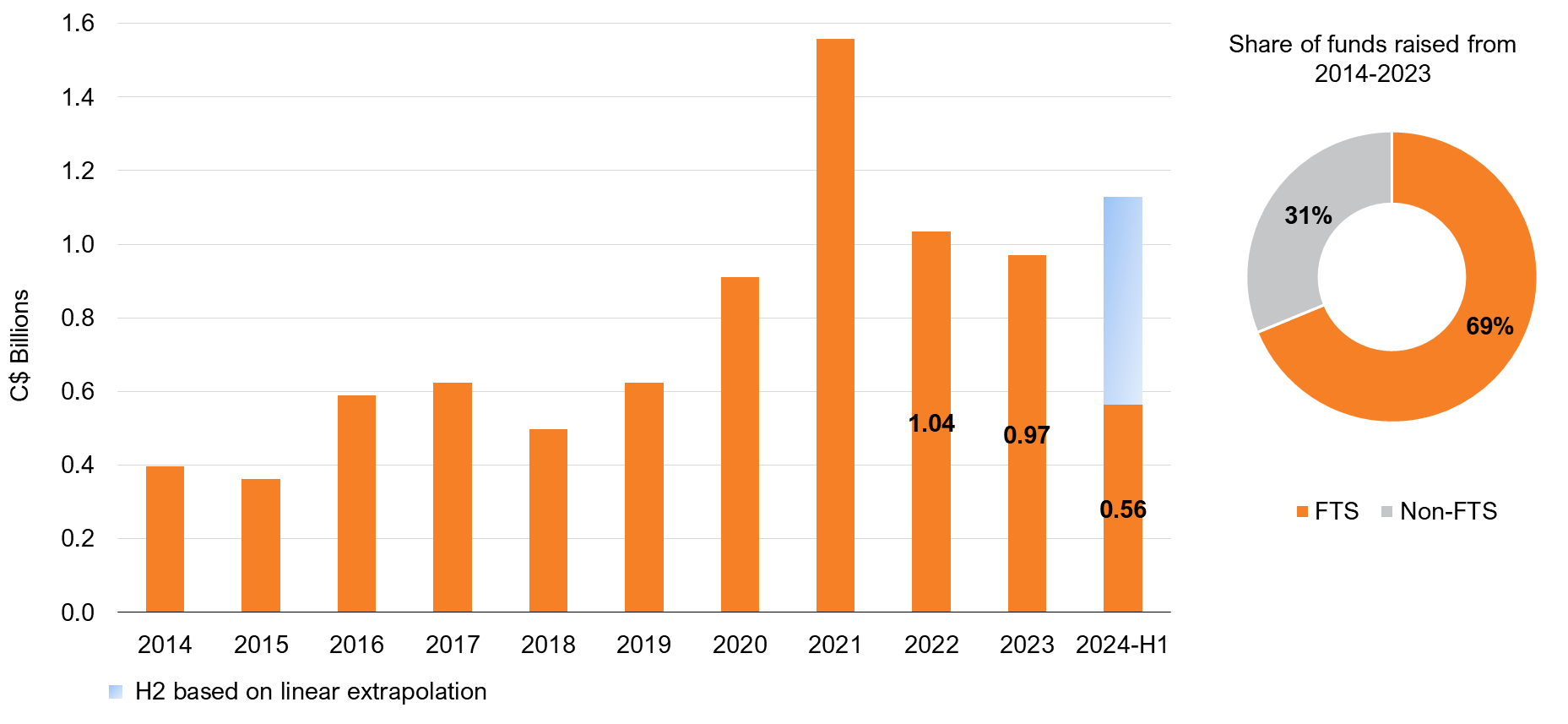

Figure 8

Figure 8 presents FTS equity raises on TSX and TSXV. The pie chart in the right hand side of the figure shows how funds were split over the past decade - FTS versus other types of equity financing, it shows that shows that over the past decade nearly 70% of the funds were raised via FTS, illustrating the crucial role this mechanism plays in incentivizing domestic exploration.

Last year, mineral explorers and developers on the TSXV raised roughly $3.3 billion (See Figure 6), with nearly one third of that coming from flow-through deals. This highlights the significant impact of the FTS regime.

The enthusiasm around critical minerals continues to grow, and we can see the influence of recent policy shifts and new incentives like the 30 per cent Critical Mineral Exploration Tax Credit (CMETC) on Canadian exploration.

Relatively high financing levels in the first half of 2024 indicate a potential for another strong year of FTS raises. However, this could be jeopardized by an increase in the capital gain inclusion rate and changes to the alternative minimum tax – which combined are expected to significantly reduce FTS availability.

Exploration Activity & Expenditures

In the last part of this report, figures 9-11 describe the current state of exploration spending.

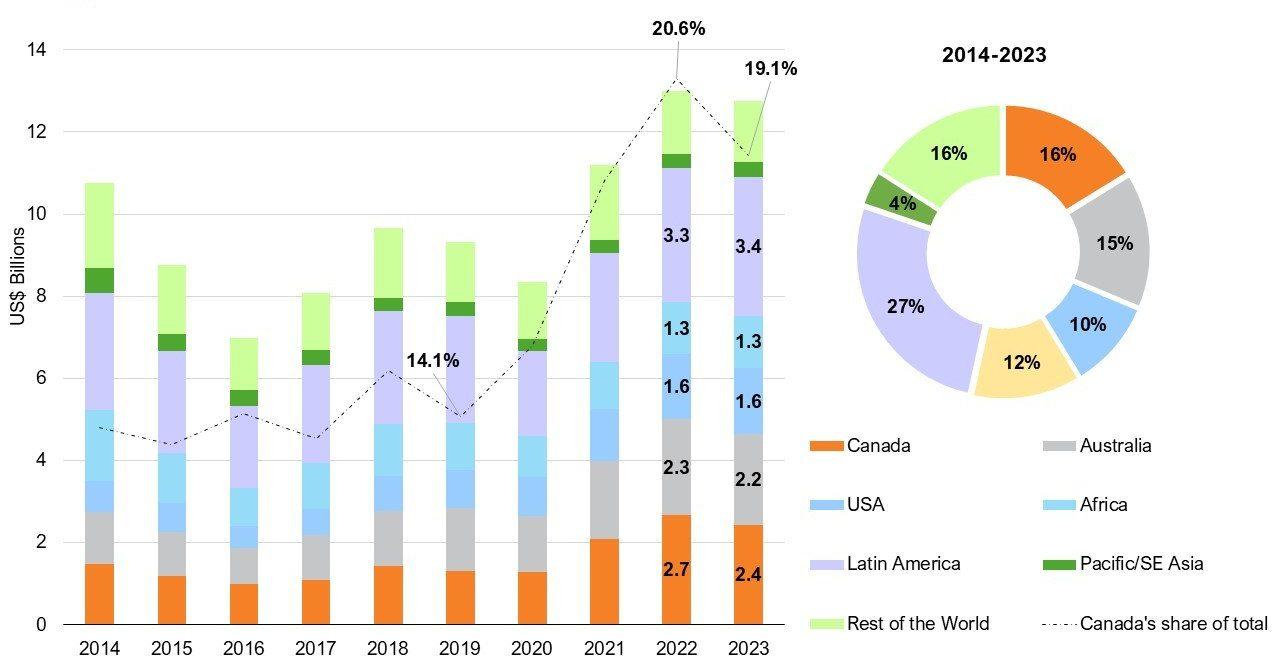

Figure 9

Figure 9 presents global exploration spending, disaggregated based on the region where the funds were spent.

After two years of increased exploration expenditures, the level of spending globally and in Canada declined modestly in 2023. This was not unexpected, given the drop in mineral sector investments in 2022.

Although Canada’s share of global exploration decreased slightly year-over-year, it still achieved the top spot for the most active mineral exploration nation in the world in 2023. This underscored the importance of Canada’s exploration incentives.

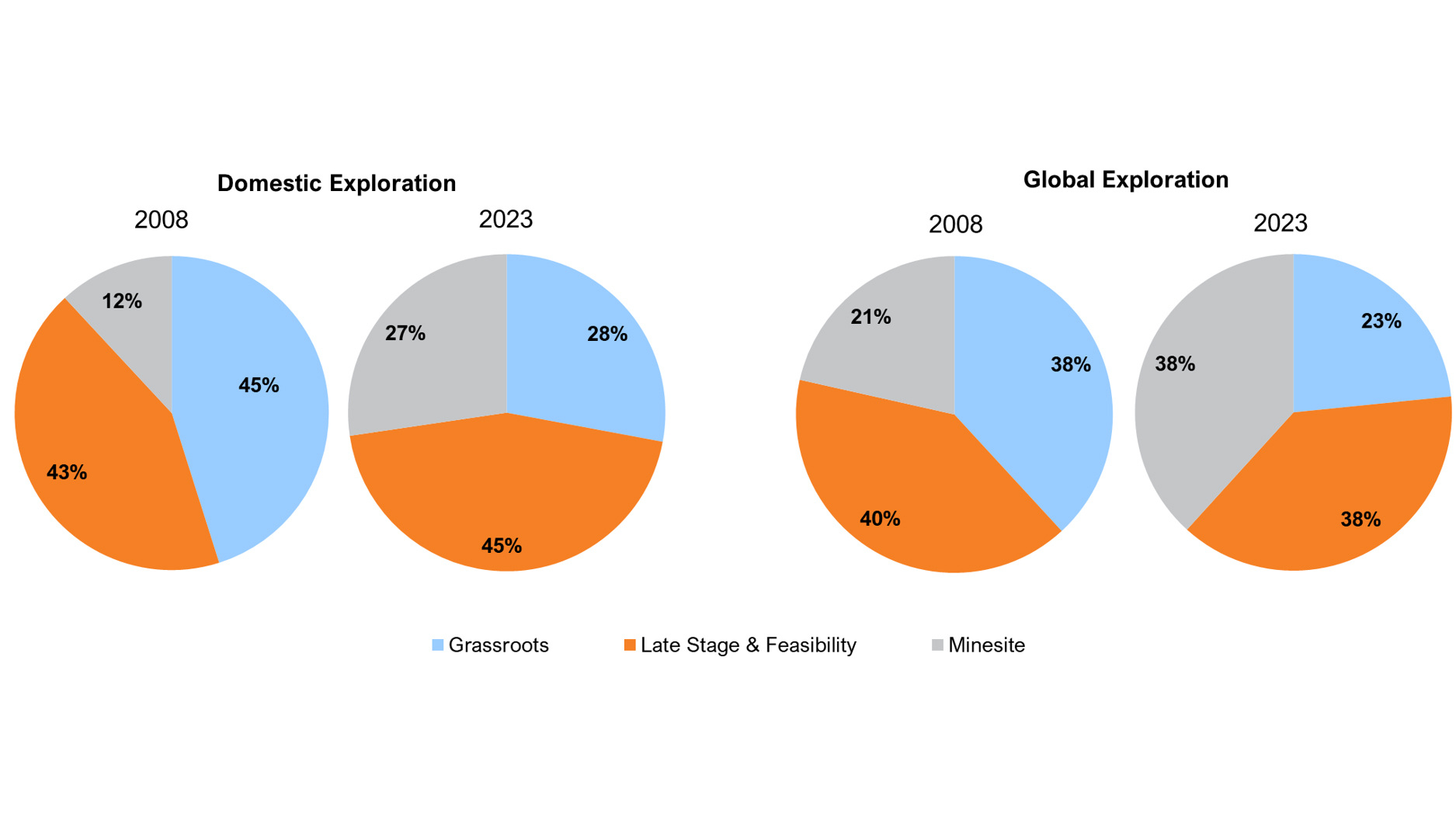

Figure 10

Figure 10 presents the distribution of global and Canadian exploration spending by project stage in 2008 vs. 2023, illustrating an alarming long-term decline in the proportion of grassroots exploration (turquoise parts of the pie charts).

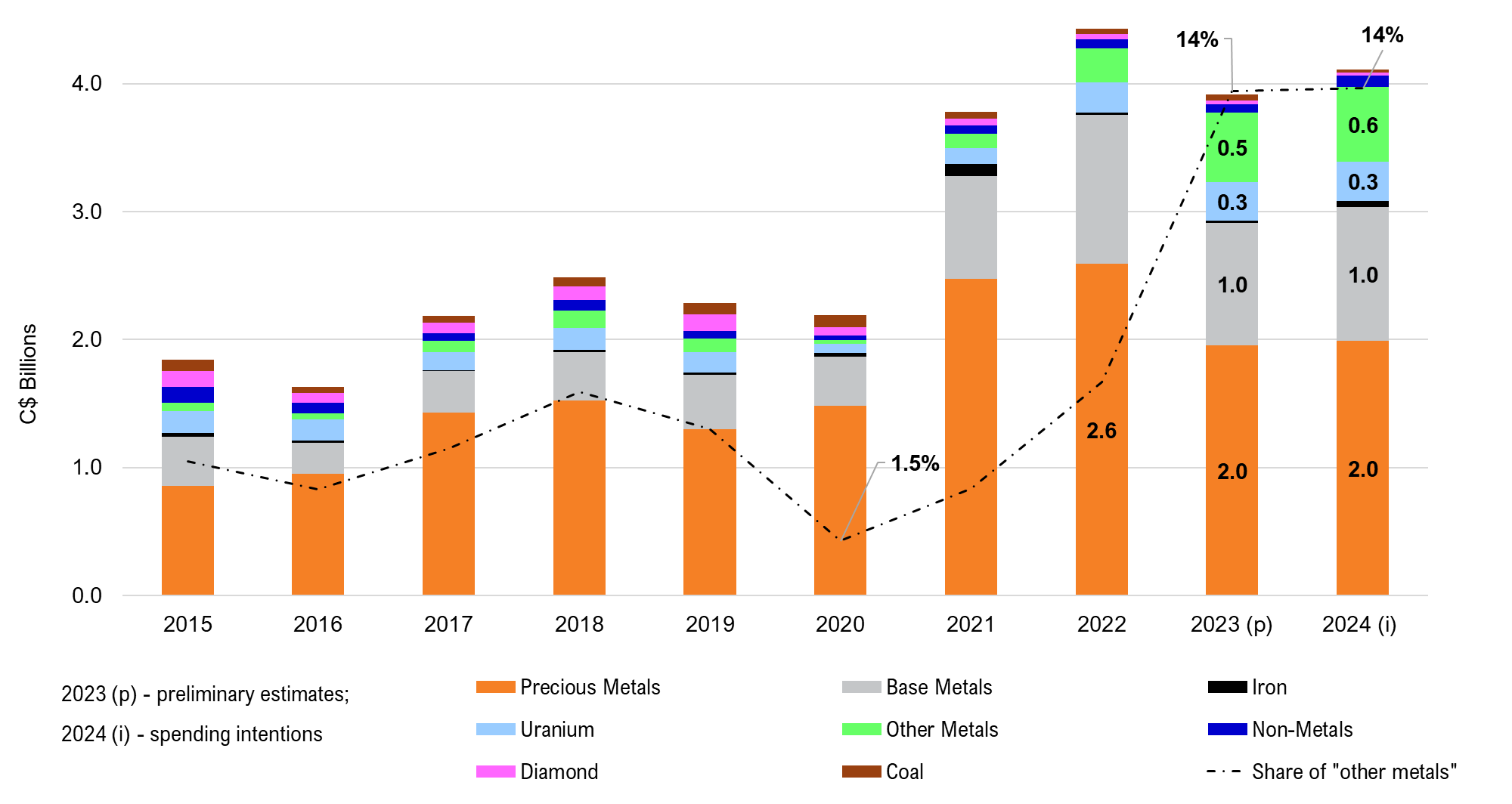

Figures 11

Lastly, Figure 11 concludes this report by outlining domestic exploration spending from 2015-2024 based on the target mineral group and illustrates some dramatic changes in the composition of sought-after commodity.

The figure shows the significant increase in exploration spending on both base and other metals.

The “Other Metals” category includes lithium, cobalt, graphite, and rare earth elements among others, and has seen an increase of more than 15 times since 2020.

This shift in focus illustrates the impact of the push towards alternative energy, international development and trade agreements for critical minerals, and targeted incentives on investment and exploration activity.

The flip side of all the new investment going into base and battery metals is that precious metals exploration dropped off substantially from 2022 to 2023 and 2024. For the first time since 2015, precious metals exploration constituted less than 50% of total activity in Canada. Despite this, more than $2 billion was still spent in Canada searching for new gold deposits in 2023 (and similar amount is expected to be spent in 2024), which is more than twice the level of activity recorded in 2015 or 2016, providing a less dire perspective on gold exploration. However, with the significant push for critical minerals exploration, it is important to remember the essential role gold exploration plays in maintaining a healthy exploration and development ecosystem in Canada.

Sources

Numbers are based on PDAC data sourced from S&P Global Market Intelligence, TMX Group, Natural Resources Canada (NRCan) and Statista.com.

Metal Prices (Figures 1-3): Metal Prices: S&P Global Market Intelligence Production data (Figure 3): Statista.com

Financing (Figures 4-8): Figure 4: S&P Global Market Intelligence Figures 5-7: TMX Group Figure 8: TMX Group, S&P Global Market Intelligence